Macroeconomics vs. Microeconomics

- Macroeconomics: study of major components of an economy (inflation, GDP, unemployment, supply and demand)

- Microeconomics: study of how households and forms make decisions and how they interact in the markets

- Positive Economics vs. Normative Economics

-Positive: tempting to describe the world as it is (ex: minimum wage causes unemployment)

-Normative: describes the worlds and how it should be, prescriptive in nature (ex: the government should raise minimum wage)

- Wants vs. Needs

-Wants: desires of citizens, much broader than our needs

-Needs: basic requirements for survival

- Scarcity: most basic fundamental economic problem that all societies face

- facing unlimited wants with limited resources

- Shortage: a situation in which quantity demand is greater than quantity supplied

- Good vs. Wants

-Goods: tangible commodities (bought, sold, traded, and produced), consumer and capital goods that are intended for final use by the consumer

-Wants: items used in the creation of other goods such as factory machinery and trucks

- Services: work that is performed for someone else

- Factors of Production (FOP)

- Land (natural resources)

- Labor

- Capital- human/physical (tools, machinery, buildings)

- Entrepreneurship

-Human capital: human made objects used to create other goods and services

-Physical capital: human made objects used to create other goods and services

- Opportunity Cost: most desirable alternative given up by making a decision

- Production Possibilities Graph (PPG), Production Possibilities Curve (PPC), Production Possibilities Frontier (PPF)

-Production Possibilities Graph: shows alternative ways to use resources

-Productive Efficiency: producing at the lowest cost, allocating resources efficiently and have full employment of resources; at any point on the curve

-Allocative Efficiency: combination of most desired by society; where to produce on the curve

- Example of Graph:

Point D: Attainable, but inefficient

Point B and A: Attainable, but efficient

Point C: Unattainable

- Law of Increasing Opportunity Cost

-When resources are shifted from making one good or service to another, the cost of producing the second item increases

-This occurs because not all resources are equally suited for the production of all goods and services

- 4 Key Assumptions of Production Possibilities

- Only two goods can be produced

- Full employment of resources

- There are fixed resources

- Fixed technology

- Demand and Supply

-Demand is the quantities that people are willing and able to buy at various prices

-The Law of Demand: there is and inverse relationship between quantity demanded

-Change in quantity demanded is caused by change in price

-Causes of "change in demand":

- Change in buyers taste (advertising)

- Change in number of buyers

- Change in income ((normal goods, inferior goods)

- Change in the price of related goods (substitute goods complimentary goods)

- Change in expectations

-Supply is the quantities that producers or sellers are willing and able to produce/sell at various prices

-The Law of Supply: there is a direct relationship between the price and quantity supplied

-Change in quantity supplied is caused by a change in price

-Causes of "change in supply":

- Change in anything except price, such as factor price

- Change in resource

- Change in technology or technique

- Change in taxes or subsidies

- Change in prices of other goods

- Change in expectations

- Change in the number of supplies

- Elasticity of Demand

-Elastic Demand: a product is elastic when demand will change greatly given a small change in price (greater than 1)

- Many substitutes

- Luxury goods

-Inelastic Demand: a product is said o be inelastic if the demand for it will not change or it changes very little regardless of price (less than 1)

- Few substitutes

- Necessary

- Calculating Elasticity Demand

- Video of Elasticity Demand In Steps

- Total Revenue

(Price)(Quantity)= Total Revenue

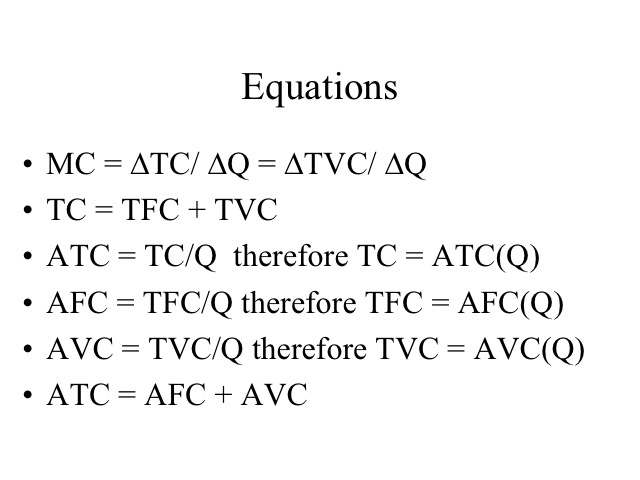

- Other Equations

- Price Floor and Price Ceiling

-Price Floor: minimum price for good or service

-Price Ceiling: maximum price that may be exchanged for good or service

- Expansion

-Real output in the economy is increasing, and the unemployment rate is deadening

-The peak is the real output at its highest point

- Recession

-Real output is decreasing, and the unemployment rate is rising

- Trough

-Lowest point of real GDP